Introduction

Budget planning is a fundamental step toward achieving and maintaining financial health. By organizing your income and expenses, you gain better control over your money, reduce stress, and work steadily toward your financial goals.

Effective budgeting strategies simplify money management by providing clear guidelines on where your money should go, helping you avoid overspending, and ensuring you’re prepared for both expected and unexpected expenses.

In this post, you will learn the key principles of budget planning, explore practical methods to track and manage your finances, and discover tools and tips that make budgeting easier and more effective.

Understanding Your Financial Situation

Calculating Your Total Monthly Income (After Taxes)

Begin by determining your total take-home pay each month—the amount you actually receive after taxes and other deductions. Include all sources of income, such as salaries, freelance work, side gigs, and any passive income streams. This provides a realistic baseline for your budgeting.

Identifying Fixed, Variable, and Irregular Expenses

To get a complete picture of your spending:

- Fixed Expenses: These are consistent monthly payments like rent, mortgage, utilities, insurance, and loan repayments.

- Variable Expenses: These fluctuate each month, such as groceries, transportation, entertainment, and dining out.

- Irregular Expenses: Costs that don’t occur monthly but must be planned for, including annual insurance premiums, holiday gifts, or car maintenance.

Importance of Honesty and Accuracy in Financial Assessment

Being truthful and precise about your income and expenses is essential. Overestimating income or underestimating expenses can lead to budget shortfalls and financial stress. Regularly reviewing and updating your financial information ensures your budget reflects reality, helping you make better decisions and stay on track.

Tracking Expenses

Methods for Tracking Spending

There are several ways to keep an eye on where your money goes:

- Apps: Budgeting apps like Mint, YNAB, or PocketGuard automatically categorize expenses and sync with your bank accounts, making tracking easy and convenient.

- Spreadsheets: Customized Excel or Google Sheets templates allow for detailed manual tracking and analysis of your spending patterns.

- Journals: Writing down every expense in a notebook or planner can increase mindfulness and help you become more aware of your spending habits.

Benefits of Consistent Tracking

- Provides a clear understanding of your spending habits and patterns.

- Helps identify unnecessary expenses and areas to cut back.

- Improves your ability to stick to your budget and achieve financial goals.

- Reduces surprises by keeping your budget realistic and up to date.

Common Pitfalls to Avoid When Tracking Expenses

- Forgetting small purchases: Minor daily expenses like coffee or snacks can add up and skew your budget if not recorded.

- Being inconsistent: Sporadic tracking reduces accuracy and usefulness. Make it a daily or weekly habit.

- Not reviewing regularly: Tracking without reviewing or adjusting your budget won’t lead to improvements.

- Neglecting cash transactions: Ensure cash expenses are logged alongside digital transactions for a full picture.

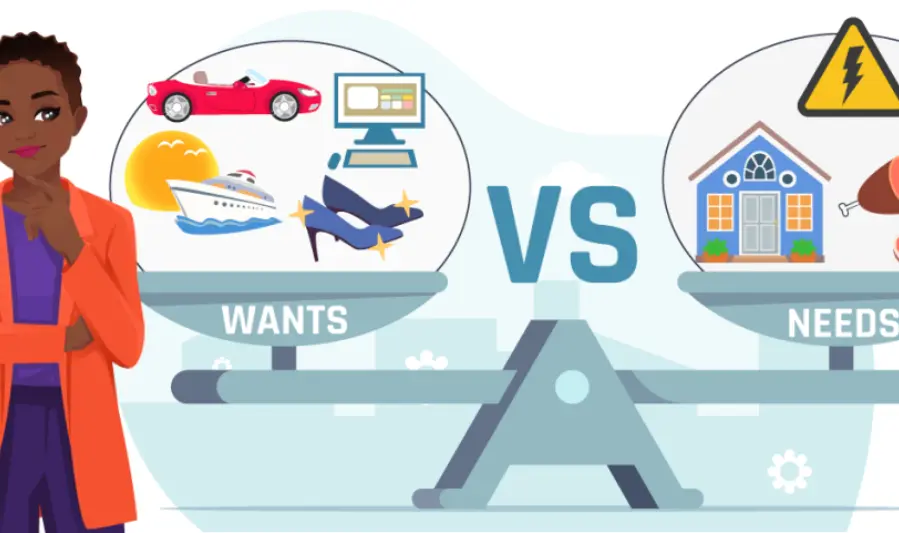

Differentiating Needs vs. Wants

Defining Essential vs. Discretionary Spending

- Needs (Essential Spending): These are expenses necessary for basic living and well-being, such as housing, utilities, food, healthcare, transportation, and education. Without these, maintaining a stable life would be difficult.

- Wants (Discretionary Spending): These are non-essential items or experiences that improve comfort or enjoyment but aren’t critical for survival. Examples include dining out, entertainment, luxury goods, and vacations.

Examples of Each Category

- Needs:

- Rent or mortgage payments

- Grocery shopping

- Utility bills (electricity, water, internet)

- Medical expenses and insurance

- School fees or childcare

- Wants:

- Cable or streaming service upgrades

- Eating at restaurants

- New clothes beyond basic needs

- Hobby supplies or gadgets

- Family vacations

Tips for Managing Wants Without Feeling Deprived

- Set a budget for discretionary spending: Allocate a reasonable amount each month specifically for wants to enjoy guilt-free spending.

- Prioritize your wants: Choose the wants that bring the most joy or value to your family and cut back on less important ones.

- Find affordable alternatives: Look for free or low-cost entertainment and activities that provide fun without overspending.

- Practice mindful spending: Pause before purchases to evaluate if the want aligns with your values and financial goals.

- Reward yourself occasionally: Allow small treats to keep motivation high while maintaining overall control.

Setting SMART Financial Goals

Explanation of SMART Goals

SMART goals are designed to make your financial objectives clear and attainable by following five criteria:

- Specific: Define exactly what you want to achieve.

- Measurable: Set criteria to track progress and know when the goal is met.

- Achievable: Ensure the goal is realistic given your current resources and constraints.

- Relevant: Align the goal with your overall financial priorities and values.

- Time-bound: Set a clear deadline to create urgency and focus.

Examples of Short-Term and Long-Term Goals

- Short-Term Goals (within 1 year):

- Save $1,000 for an emergency fund in 6 months by saving $167 monthly.

- Pay off a credit card balance of $500 within 4 months.

- Long-Term Goals (over 1 year):

- Save $20,000 for a down payment on a house in 5 years by saving $333 monthly.

- Build a college fund of $50,000 in 10 years by investing regularly.

How to Prioritize Multiple Goals

- Rank by urgency: Focus first on goals that protect your financial health, like emergency savings or debt repayment.

- Consider impact: Prioritize goals that have the biggest positive effect on your family’s future.

- Balance short and long term: Allocate resources so you make progress on immediate needs and long-term aspirations simultaneously.

- Review and adjust: Regularly revisit your goals to reflect changes in your financial situation or priorities.

Choosing a Budgeting Method

Popular Budgeting Methods

1. 50/30/20 Rule

- Overview: Divide your after-tax income into three broad categories:

- 50% for needs (housing, groceries, bills)

- 30% for wants (dining out, entertainment, hobbies)

- 20% for savings and debt repayment

- Pros: Simple to understand and implement; flexible for different income levels; easy for families new to budgeting.

- Cons: May be too broad for families with complex or fluctuating expenses; not ideal for tight budgets needing detailed tracking.

2. Zero-Based Budgeting

- Overview: Every dollar of income is assigned a specific purpose, so income minus expenses equals zero. This means you plan exactly how every dollar is spent or saved each month.

- Pros: Provides detailed control and awareness of spending; maximizes efficient use of income; helps eliminate waste.

- Cons: Can be time-consuming and require constant updates; may feel overwhelming for busy families.

3. Envelope System

- Overview: Allocate cash (or digital equivalents) into envelopes labeled for spending categories (e.g., groceries, childcare, utilities). Spend only what’s in each envelope for the month.

- Pros: Great for controlling discretionary spending; tactile and visual method that can help curb overspending.

- Cons: Managing cash envelopes can be inconvenient; less suited for digital or automated payments; requires discipline to avoid borrowing from other envelopes.

How to Select the Best Fit for Your Lifestyle

- Assess your family’s financial complexity: For simple, steady incomes, 50/30/20 works well; for variable income or detailed needs, zero-based budgeting may be better.

- Consider your family’s comfort with budgeting tools: Some prefer digital apps for automation, others like tangible methods like envelopes.

- Factor in time and consistency: Choose a method you can realistically maintain without causing burnout.

- Combine methods if needed: For example, use 50/30/20 as a framework and envelopes for specific categories that tend to overspend.

- Involve your family: Get input from all members who manage or influence spending to ensure buy-in and practicality.

Building and Maintaining an Emergency Fund

Why Emergency Funds Are Crucial

An emergency fund acts as a financial safety net for unexpected expenses such as medical emergencies, car repairs, or sudden loss of income. It prevents the need to rely on high-interest debt and provides peace of mind, helping families stay financially stable during tough times.

How to Start Small and Grow the Fund

- Start with a modest goal: Aim for an initial $500 to $1,000 to cover minor emergencies.

- Set monthly savings targets: Break down your ultimate goal (typically 3–6 months of essential expenses) into manageable monthly amounts.

- Automate savings: Set up automatic transfers to your emergency fund account to build it steadily without extra effort.

- Add windfalls: Use bonuses, tax refunds, or gifts to boost your emergency savings faster.

Best Places to Keep Emergency Savings

- High-Yield Savings Accounts: Offer easy access with better interest rates than regular savings accounts.

- Money Market Accounts: Provide competitive interest and liquidity, suitable for emergency funds.

- Short-Term CDs (Certificates of Deposit): Can be part of the fund if you keep a portion liquid; be mindful of withdrawal penalties.

you may also like to read these posts:

Powerful & Compact: Best Portable Mini PCs for

Paghahanda para sa Pagsusulit: Gabay at Tips

Gabay Aral para sa mga Mag-aaral sa Elementarya

Rozmarra ki Budget Tips jo Asar Dikhayein

Automating Finances

Benefits of Automating Savings and Bill Payments

- Consistency: Automation ensures you regularly save and pay bills on time without relying on memory or discipline.

- Time-saving: Reduces the effort of manual payments and transfers, freeing up time for other priorities.

- Avoids late fees: Automatic bill payments help prevent missed payments and penalties.

- Builds savings effortlessly: Automated transfers to savings accounts or investments make it easier to grow your emergency fund or reach financial goals.

How to Set Up Automation Effectively

- Prioritize your goals: Decide which bills and savings goals to automate first—typically essential bills and emergency fund contributions.

- Choose reliable tools: Use your bank’s online banking platform or trusted budgeting apps that offer automation features.

- Schedule around payday: Set transfers and payments to occur shortly after your income deposits to ensure sufficient funds.

- Monitor regularly: Even with automation, review your accounts monthly to ensure payments are processed and adjust amounts as needed.

Avoiding Common Automation Pitfalls

- Overdraft risks: Make sure your accounts have enough funds to cover automated payments to avoid overdraft fees.

- Ignoring changes: Keep track of changes in bills or savings goals and update automation settings accordingly.

- Lack of oversight: Don’t set it and forget it completely—regularly check your statements to catch errors or fraudulent charges.

- Over-automation: Avoid automating too many small payments that complicate your finances; keep some flexibility for discretionary spending.

Regular Budget Review and Adjustments

Why Monthly Reviews Are Important

Reviewing your budget monthly helps you stay on track with your financial goals, catch any discrepancies early, and adapt to changes. It reinforces good habits, prevents overspending, and ensures your budget reflects your current reality.

What to Look for During a Review

- Compare planned vs. actual spending: Identify categories where you overspent or underspent.

- Track progress on goals: See if you’re meeting your savings targets or debt repayment plans.

- Notice irregular expenses: Account for one-time or seasonal costs that might affect future budgets.

- Evaluate income changes: Consider any raises, bonuses, or drops in income.

How to Adjust Your Budget Based on Life Changes

- Update income and expenses: Reflect new income sources, bills, or lifestyle changes promptly.

- Reprioritize goals: Shift focus if urgent needs arise, such as emergency funds or debt payoff.

- Modify spending limits: Increase or decrease allocations for categories like groceries or entertainment as needed.

- Communicate with family: Ensure everyone is aware of adjustments and involved in the process.

Avoiding Common Budgeting Mistakes

Overlooking Small Expenses

Small, frequent purchases—like coffee, snacks, or subscriptions—can add up quickly and derail your budget if ignored. Make sure to track even minor expenses to get an accurate picture of your spending.

Ignoring Irregular or Seasonal Costs

Expenses such as annual insurance premiums, holiday gifts, or seasonal maintenance often catch people off guard. Plan ahead by estimating these costs and setting aside money monthly to cover them.

Being Too Rigid or Unrealistic

Budgets should be flexible enough to accommodate unexpected changes or occasional treats. Setting overly strict limits can lead to frustration and give up on budgeting altogether. Aim for a balanced approach that allows for adjustments.

Not Involving Others in the Budgeting Process

When budgeting for families or households, excluding partners or family members can cause misunderstandings and reduce commitment to financial goals. Engage everyone involved to promote teamwork and transparency.

Faqs:

What is the best budgeting method for beginners?

The 50/30/20 rule is often recommended for beginners because it’s simple and flexible, dividing income into needs, wants, and savings.

How can I stick to my budget without feeling restricted?

Include a reasonable amount for discretionary spending and focus on your financial goals. Flexibility and realistic planning help maintain motivation.

How often should I review my budget?

Review your budget monthly to track progress and make necessary adjustments based on changes in income, expenses, or goals.

What should I do if I overspend one month?

Don’t be discouraged. Analyze what caused the overspending, adjust your budget if needed, and get back on track the following month.

Can budgeting help me pay off debt faster?

Yes, budgeting helps you allocate extra funds toward debt repayment, prioritize high-interest debts, and avoid accumulating new debt.

Conclusion

Effective budget planning is the cornerstone of financial success. By understanding your income and expenses, setting realistic goals, and choosing the right budgeting methods, you can take control of your finances and reduce financial stress. Remember, budgeting is not about restriction but about making intentional choices that align with your priorities. Stay consistent, review your progress regularly, and be flexible enough to adjust as life changes. With these strategies in place, you’re well on your way to achieving greater financial stability and long-term prosperity.