Introduction

Budget planning is a crucial skill for every family aiming to maintain financial stability and achieve their long-term goals. With multiple members relying on a single income or combined earnings, managing money wisely becomes even more important. Effective budgeting helps families ensure that essential needs are met, debts are managed, and future plans—such as education, vacations, or retirement—are within reach.

Families face unique financial challenges, including fluctuating expenses like childcare, school supplies, healthcare costs, and unexpected emergencies. Balancing these demands while saving for both short-term needs and long-term goals requires careful planning and regular review.

This guide will walk you through the essential steps of family budget planning. You’ll learn how to assess your income and expenses, prioritize spending, set realistic financial goals, and involve all family members in maintaining a healthy financial routine. By the end, you’ll be equipped with practical tools and strategies to create a budget that supports your family’s present needs and future dreams.

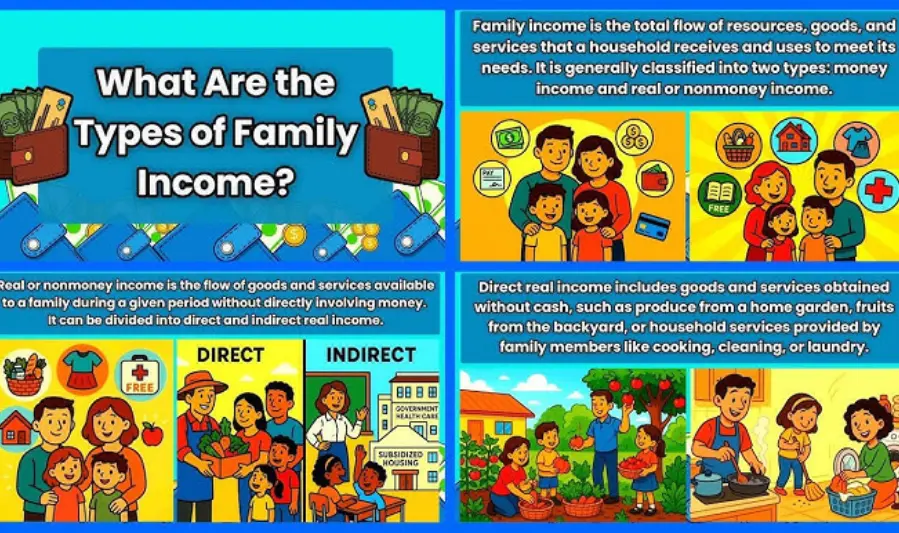

Understanding Family Income

Identifying All Sources of Family Income

For effective budgeting, it’s essential to have a complete picture of your family’s total income. This includes:

- Salaries and wages from all working family members

- Bonuses, commissions, or overtime pay

- Income from freelance work, side hustles, or part-time jobs

- Passive income sources such as rental properties, dividends, or interest

- Government benefits or child support payments

Having a clear list of all income sources ensures your budget is accurate and comprehensive.

Managing Fluctuating or Irregular Income

Many families face income that isn’t consistent every month, such as freelance payments, commissions, or seasonal work. To manage this:

- Calculate an average monthly income based on several months of earnings.

- Use a conservative estimate to avoid overestimating what you have available.

- Prioritize covering fixed expenses first, then allocate remaining funds to savings or variable costs.

- Consider creating a buffer or emergency fund to cushion months when income is lower.

Importance of Honest and Realistic Income Assessment

Being honest about your actual income helps avoid budgeting mistakes and financial stress. Overestimating income can lead to overspending, while underestimating may cause unnecessary restrictions. Regularly reviewing and updating your income information ensures your budget reflects your true financial situation and supports better decision-making.

Comprehensive Expense Tracking

Types of Expenses: Fixed, Variable, and Irregular

To create an effective family budget, it’s important to understand the different types of expenses:

- Fixed Expenses: These are regular, predictable costs that stay mostly the same each month, such as rent or mortgage payments, utilities, insurance premiums, and loan repayments.

- Variable Expenses: These fluctuate monthly and include groceries, transportation, entertainment, and dining out. While more flexible than fixed expenses, tracking these helps identify areas to adjust.

- Irregular Expenses: Costs that don’t occur every month but need to be planned for, such as annual subscriptions, school fees, medical bills, holiday gifts, or car maintenance.

How to Track Expenses Effectively

Keeping track of expenses accurately is key to understanding your spending habits and making informed adjustments. Here are some methods:

- Apps: Use budgeting apps like Mint, YNAB, or Goodbudget that categorize and track expenses automatically.

- Spreadsheets: Customize your own tracking sheets using Excel or Google Sheets for detailed control.

- Envelope System: Use physical or digital envelopes to allocate money to different spending categories, which helps control spending by limiting what’s available.

Importance of Involving the Whole Family in Tracking

Getting everyone involved—spouses, partners, and even older children—creates transparency and shared responsibility. When the whole family understands the budget and contributes to tracking expenses, it promotes better financial habits, reduces surprises, and encourages teamwork in achieving financial goals.

Needs vs. Wants in a Family Context

Defining Essential vs. Non-Essential Family Expenses

In family budgeting, distinguishing between needs and wants is vital to prioritize spending effectively.

- Needs are necessary expenses that support the family’s basic well-being and functioning. These include housing, utilities, groceries, healthcare, education, and transportation.

- Wants are discretionary expenses that enhance comfort or enjoyment but aren’t essential for daily living. Examples include dining out, vacations, entertainment subscriptions, and luxury items.

Examples Specific to Families

- Needs:

- Childcare or daycare fees

- School supplies and tuition (if applicable)

- Extracurricular activities that contribute to child development (sports, music lessons)

- Medical expenses and insurance premiums

- Wants:

- New gadgets or toys

- Family vacations or frequent dining out

- Upgraded cable packages or streaming services beyond basic needs

Strategies to Reduce Wants Without Sacrificing Family Happiness

- Set spending limits: Allocate a specific monthly budget for discretionary spending that everyone agrees on.

- Find low-cost or free alternatives: Explore community events, parks, and activities that provide fun without a high price tag.

- Prioritize meaningful experiences: Focus spending on activities that create lasting memories rather than material items.

- Practice mindful spending: Encourage family members to pause before purchases and discuss if the expense truly adds value.

- Rotate “wants”: Instead of cutting all wants, alternate which activities or items to enjoy each month, keeping things balanced.

Setting Family Financial Goals

How to Set SMART Goals for Families

SMART goals are Specific, Measurable, Achievable, Relevant, and Time-bound—a framework that helps families create clear and actionable financial targets. For example, instead of saying “save more money,” a SMART goal would be:

“Save $3,000 for a family vacation within 12 months by setting aside $250 each month.”

Using SMART criteria ensures goals are realistic and progress is easy to track.

Short-Term vs. Long-Term Family Goals

- Short-Term Goals: These are objectives you aim to accomplish within a year or less, such as:

- Building an emergency fund

- Paying off a credit card

- Saving for school supplies or holiday gifts

- Long-Term Goals: These take several years or more to achieve and often require consistent planning, such as:

- Saving for your children’s college education

- Buying a home

- Planning for retirement

Both short-term and long-term goals are important and should complement each other in your family’s financial plan.

Prioritizing Goals Based on Family Values and Situation

Every family’s priorities are unique. When setting goals, consider:

- What matters most to your family: Education, security, experiences, or debt freedom?

- Current financial situation: Focus first on goals that address urgent needs like emergency savings or debt reduction.

- Involvement of family members: Include everyone in discussions to ensure goals reflect shared values and foster teamwork.

Prioritizing goals helps allocate resources wisely and keeps the whole family motivated.

Choosing the Right Budgeting Method for Families

Detailed Explanation of Budgeting Methods

- 50/30/20 Rule:

This simple rule divides your after-tax income into three categories:- 50% for needs (housing, groceries, utilities)

- 30% for wants (dining out, entertainment, vacations)

- 20% for savings and debt repayment

- Envelope System:

This method involves allocating cash (or digital equivalents) into envelopes labeled for specific spending categories (e.g., groceries, kids’ activities, utilities). Once the money in an envelope is gone, no more spending is allowed in that category until the next budget period. - Zero-Based Budgeting:

Every dollar of income is assigned a job, whether it’s paying bills, saving, or spending. The goal is for your income minus expenses to equal zero at the end of the month. This method requires detailed tracking and planning but maximizes control over finances.

Pros and Cons of Each Method for Families

| Method | Pros | Cons |

|---|---|---|

| 50/30/20 Rule | Easy to understand and implement; flexible | May oversimplify complex family budgets |

| Envelope System | Helps control spending; great for variable expenses | Requires discipline; less convenient for digital payments |

| Zero-Based Budgeting | Offers full control and detailed awareness | Time-consuming; can be overwhelming for busy families |

Tips for Customizing a Method to Fit Your Family’s Lifestyle

- Consider your family’s financial goals, income stability, and spending habits.

- Combine methods if needed — for example, use the 50/30/20 framework alongside envelopes for discretionary spending.

- Involve family members in budgeting discussions to ensure buy-in and realistic allocations.

- Use digital tools or apps to simplify tracking, especially for busy households.

- Revisit and adjust your method regularly as family needs and circumstances change.

Building and Maintaining an Emergency Fund

Why Emergency Funds Are Crucial for Families

Families often face unexpected expenses such as medical emergencies, car repairs, or sudden job loss. An emergency fund provides a financial cushion that helps cover these costs without derailing your budget or forcing you into debt. It ensures your family’s basic needs are met during difficult times and reduces financial stress.

How to Start and Grow the Fund Gradually

- Start Small: Begin by saving a modest amount, such as $500 to $1,000, to cover minor emergencies.

- Set Realistic Goals: Aim to eventually save enough to cover 3 to 6 months of essential living expenses, including housing, food, utilities, and childcare.

- Automate Savings: Set up automatic transfers to your emergency fund account each month to build it consistently without extra effort.

- Use Windfalls: Consider adding bonuses, tax refunds, or gifts to your emergency fund to accelerate growth.

Where to Keep the Emergency Fund for Accessibility and Growth

Your emergency fund should be:

- Easily Accessible: You need quick access during emergencies without penalties or delays.

- Safe: Avoid risky investments that could lose value.

Good places to keep your emergency fund include: - High-Yield Savings Accounts: Offer better interest rates than regular savings accounts while allowing easy access.

- Money Market Accounts: Provide competitive interest and liquidity.

- Short-Term Certificates of Deposit (CDs): Can be considered if you keep part of the fund liquid, but be aware of withdrawal restrictions.

you may also like to read these posts:

Powerful & Compact: Best Portable Mini PCs for

Paghahanda para sa Pagsusulit: Gabay at Tips

Gabay Aral para sa mga Mag-aaral sa Elementarya

Rozmarra ki Budget Tips jo Asar Dikhayein

Effective Family Communication and Budget Meetings

How to Conduct Monthly or Quarterly Family Budget Meetings

- Set a regular schedule: Choose a consistent time each month or quarter for the family to gather and review the budget.

- Prepare in advance: Collect financial statements, bills, and updates on goals beforehand to keep the meeting focused and productive.

- Review income and expenses: Discuss how the family is doing compared to the budget, celebrate successes, and identify any challenges.

- Plan for upcoming expenses: Talk about upcoming bills, events, or large purchases to adjust the budget accordingly.

- Set or revise goals: Use these meetings to update financial goals based on progress and changes in circumstances.

Involving Children and Teenagers in Money Discussions

- Age-appropriate conversations: Tailor discussions to your children’s understanding, teaching basic money concepts early and involving teens in more detailed planning.

- Encourage questions: Create a safe space for kids to ask about money, savings, and spending.

- Assign responsibilities: Give older children small money tasks or allowances to practice budgeting and decision-making.

- Lead by example: Show healthy financial habits in your discussions and actions.

Handling Disagreements and Fostering Teamwork

- Listen actively: Make sure everyone’s views and concerns are heard without judgment.

- Stay solution-focused: Instead of blaming, work together to find compromises and adjust the budget to meet shared priorities.

- Set family financial values: Agree on common goals and principles to guide spending and saving decisions.

- Celebrate teamwork: Recognize when the family works well together financially, reinforcing positive behavior.

Faqs:

How can a family with a single income effectively budget their expenses?

Focus on prioritizing essential expenses first, track every cost carefully, and look for ways to increase income or reduce discretionary spending. A clear budget helps manage resources wisely.

What is the best way to include children’s expenses in the family budget?

Include regular costs like schooling, clothing, and activities under fixed or variable expenses. Also, allocate a small budget for kids’ personal spending to teach them money management.

How should families handle unexpected or emergency expenses?

Build an emergency fund gradually with a goal of 3–6 months’ worth of essential expenses. When emergencies arise, use this fund to avoid disrupting your monthly budget.

What if one partner isn’t willing to participate in budgeting?

Open, honest communication is key. Discuss financial goals together, highlight the benefits of budgeting, and consider compromises or seeking professional advice if needed.

How often should families review and update their budget?

Review your budget monthly to track progress and adjust for changes in income, expenses, or goals. Regular meetings keep everyone aligned and accountable.

Conclusion

Budget planning is a vital tool that helps families manage their finances effectively, reduce stress, and work together toward shared financial goals. By understanding your income, tracking expenses, distinguishing between needs and wants, and maintaining open communication, your family can build a strong financial foundation. Remember, the key to successful budgeting is consistency and teamwork. Start small, stay flexible, and make budgeting a regular part of your family’s routine. With time, patience, and cooperation, your family can achieve financial stability and create a secure future together.