Introduction

Investing is one of the most powerful tools for building long-term wealth, and starting early can make a significant difference thanks to the power of compound growth. Whether you’re a student, a young professional, or simply new to the world of investing, taking the first step early can help you reach your financial goals faster and with less effort over time.

However, many beginners feel overwhelmed by the idea of investing. Common fears include losing money, not understanding how investments work, or thinking they need a lot of money to get started. These concerns are valid—but the truth is, there are beginner-friendly, low-risk investment options that can help ease you into the process without requiring advanced financial knowledge or large amounts of capital.

In this post, you’ll learn about some of the best low-risk investment options for beginners. We’ll break down how each one works, why it may be a good fit for new investors, and how to get started—even with a modest budget.

Why Should Beginners Start Investing?

1. The Effect of Inflation on Savings

While saving money is essential, simply leaving your funds in a traditional savings account can actually reduce their value over time. This is due to inflation—the gradual increase in the cost of goods and services.

If your savings earn 1% interest but inflation rises by 3%, you’re effectively losing purchasing power. Investing helps your money grow at a rate that can outpace inflation, preserving and increasing its value.

2. The Power of Compound Interest

Investing early allows you to take full advantage of compound interest—earning interest not just on your initial investment, but also on the interest it accumulates over time.

For example, investing $1,000 at a 7% annual return for 30 years could grow to over $7,600 without any additional contributions. The longer your money stays invested, the more dramatic the effect of compounding becomes.

3. Saving vs. Investing

- Saving is setting aside money for short-term needs or emergencies, typically in low-risk accounts like savings or money market accounts.

- Investing is using your money to buy assets (like stocks, bonds, or funds) that have the potential to grow over time.

While saving is safe, investing is necessary for long-term growth and wealth-building. A healthy financial plan includes both.

4. Long-Term Benefits of Early Investing

The earlier you start investing, the more time your money has to grow. Starting in your 20s—even with small amounts—can yield far greater returns than starting later with more money.

Early investing can help you:

- Retire comfortably

- Afford large future expenses (home, education, travel)

- Become financially independent sooner

Key Principles Every Beginner Should Know

Before putting your money into any investment, it’s essential to understand a few foundational principles. These will help you make smarter decisions, manage risk, and align your investments with your life goals.

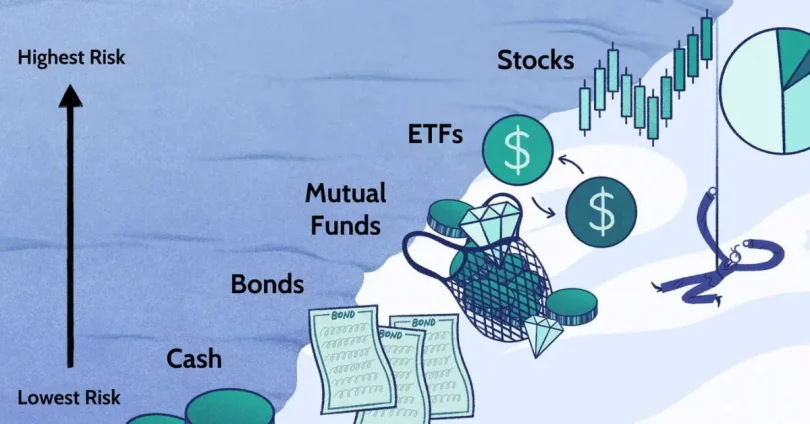

1. Risk vs. Reward

All investments carry some level of risk. Generally, the higher the potential return, the higher the risk involved.

- Low-risk investments (e.g., bonds, savings accounts) offer more stability but lower returns.

- High-risk investments (e.g., individual stocks, crypto) can bring higher returns, but also greater losses.

Understanding your personal risk tolerance will help you choose investments that feel comfortable and appropriate for your situation.

2. Diversification

“Don’t put all your eggs in one basket.” Diversification means spreading your money across different types of investments (stocks, bonds, funds, etc.) and sectors.

It reduces the impact of a poor-performing asset and helps balance risk in your portfolio.

3. Time Horizon

Your time horizon is how long you plan to keep your money invested before needing it.

- Short-term goals (1–3 years): Choose low-risk, liquid investments.

- Long-term goals (5+ years): You can afford to take more risk since there’s time to recover from market fluctuations.

The longer your time horizon, the more growth potential your investments can have.

4. Setting Financial Goals

Investing without a goal is like driving without a destination. Are you investing to buy a house, fund your retirement, or build wealth in general?

Clear goals help you decide:

- How much to invest

- What kind of assets to choose

- When to adjust your strategy

5. Emergency Fund First, Investing Second

Before you start investing, it’s wise to have an emergency fund—usually 3 to 6 months’ worth of living expenses saved in a liquid, low-risk account.

This ensures you won’t be forced to pull money out of your investments early (which could result in losses or penalties) if an unexpected expense arises.

High‑Yield Savings Accounts

- Risk level: Very low (virtually risk-free in many jurisdictions)

- Pros:

- Easy to access and understand

- Keeps funds liquid and safe

- Better interest rates than traditional savings accounts

- Cons:

- Very modest returns compared to investing in markets

- Returns may barely outpace inflation

- Minimum investment: Often very low (sometimes just a few dollars or local equivalent)

- Ideal time horizon: Short‑term (3 months to a few years)

- Beginner tip: Use this as a place to hold your emergency fund or funds you may need soon, before moving into higher‑risk investments.

b. Certificates of Deposit (CDs)

- Risk level: Low

- Pros:

- Fixed interest rate for a defined term

- Predictable (you know what you’ll get)

- Cons:

- Money is locked in for the term; early withdrawal usually incurs penalties

- Returns are relatively low compared to market investments

- Minimum investment: Varies; depends on bank or institution (could be $500 or more)

- Ideal time horizon: Short‑ to medium‑term (typically months to a few years)

- Beginner tip: Use CDs for money you won’t need immediately and want to preserve with minimal risk.

c. Index Funds

- Risk level: Moderate (market risk exists, but spread across many stocks)

- Pros:

- Broad diversification (many stocks in one fund)

- Low fees (especially for passive index funds)

- Good for long‑term growth

- Cons:

- Value can fluctuate with market ups and downs

- Requires patience; short‑term returns can be volatile

- Minimum investment: Some funds allow small amounts; depends on broker/fund

- Ideal time horizon: Medium to long term (5‑10+ years)

- Beginner tip: Consider low‑cost funds that track broad markets and try dollar‑cost averaging (invest regularly) rather than trying to time the market.

d. ETFs (Exchange‑Traded Funds)

- Risk level: Similar to index funds—moderate, depends on underlying assets

- Pros:

- Flexibility: trade like stocks, diversified like funds

- Often lower fees than mutual funds

- Cons:

- Market fluctuations can impact value

- Some ETFs may track niche or riskier assets—must check what’s inside

- Minimum investment: Often the price of 1 share (or even fractional shares)

- Ideal time horizon: Medium to long term

- Beginner tip: Choose broadly diversified ETFs (e.g., total market or global) to spread risk, rather than narrow or speculative ones.

e. Mutual Funds

- Risk level: Varies widely (depends on what the fund invests in)

- Pros:

- Professionally managed

- Diversified across many assets

- Accessible to beginners

- Cons:

- Some have higher fees

- Minimums may be higher in some cases

- Minimum investment: Varies (some programs allow small monthly amounts)

- Ideal time horizon: Medium to long term

- Beginner tip: Look for funds with low expense ratios and clear objectives. Know whether the fund is mostly stocks (higher risk) or bonds (lower risk).

f. Robo‑Advisors

- Risk level: Moderate (varies with your risk profile)

- Pros:

- Automated, beginner‑friendly platforms

- Often low minimums and low fees

- Portfolios tailored to your risk tolerance

- Cons:

- You have less direct control if you want to pick individual investments

- Fees still exist (though generally low)

- Minimum investment: Often very low (some start at $100 or less)

- Ideal time horizon: Medium to long term

- Beginner tip: Great for first‑time investors who want simplicity and automation rather than managing every detail.

g. Individual Stocks

- Risk level: High (can gain a lot, can also lose a lot)

- Pros:

- Potential for high returns

- Opportunity to invest in companies you believe in

- Cons:

- Requires more research and monitoring

- Less diversification unless you buy many different stocks

- Minimum investment: Depends on stock price (some allow fractional shares)

- Ideal time horizon: Long term (5+ years)

- Beginner tip: Start small, diversify, and consider stocks as only a portion of your portfolio rather than your entire investment.

h. REITs (Real Estate Investment Trusts)

- Risk level: Moderate to high (depends on market and property sector)

- Pros:

- Exposure to real estate without buying property

- Often pays regular dividends

- Cons:

- Real estate market fluctuations affect REITs

- Fees and tax considerations may apply

- Minimum investment: Price of one share (can be reasonable)

- Ideal time horizon: Medium to long term

- Beginner tip: Use REITs to diversify outside of just stocks/bonds, but keep in mind they still carry risks and you need to understand the underlying assets.

i. Government Bonds

- Risk level: Low to moderate (depending on country and term)

- Pros:

- Predictable income (interest payments)

- Relatively safe compared to equities

- Cons:

- Returns are often lower

- Inflation may reduce real returns

- Minimum investment: Varies greatly by country and bond type

- Ideal time horizon: Depending on bond term—short, medium, or long term

- Beginner tip: Good for stability in a portfolio. Use bonds to balance riskier assets like stocks.

j. Retirement Accounts (401(k), IRA, Roth IRA)

- Risk level: Varies (depends on what assets you hold inside)

- Pros:

- Tax advantages (depending on account type)

- Encourages long‑term investing and discipline

- Cons:

- Money may be locked in until certain age—early withdrawal may incur penalty

- Requires understanding account rules and fees

- Minimum investment: Depends on plan/provider (sometimes very low or none)

- Ideal time horizon: Very long term (decades)

- Beginner tip: If available, take advantage of employer match (if you have 401(k) or similar) and choose low‑cost funds inside the retirement account. Starting early gives you maximum benefit from compounding.

Summary Comparison

| Investment Type | Risk | Time Horizon | Best For |

|---|---|---|---|

| High‑Yield Savings | Very Low | Short term | Emergency fund, savings goal |

| CDs | Low | Short to medium | Safe preservation of funds |

| Index Funds | Moderate | Medium to long | Beginners wanting growth |

| ETFs | Moderate | Medium to long | Flexible, diversified investing |

| Mutual Funds | Moderate | Medium to long | Beginners wanting managed diversification |

| Robo‑Advisors | Moderate | Medium to long | Beginners wanting automation |

| Individual Stocks | High | Long term | More experienced, higher risk appetite |

| REITs | Moderate‑High | Medium to long | Diversification into real estate |

| Government Bonds | Low–Moderate | Short to long | Stability, income generation |

| Retirement Accounts | Varies | Very long | Long‑term savings & tax benefits |

Final Thoughts for Beginners:

- Focus on low‑ to moderate‑risk options until you’re comfortable.

- Diversify your portfolio rather than betting on one type of investment.

- Invest regularly (even small amounts) rather than waiting to “have enough”.

- Match investments to your time horizon and goals—money you’ll need soon should be in safer places; long‑term money can take more risk.

- Take advantage of tax‑efficient accounts (if available in your country) and be aware of fees.

How to Choose the Right Investment Option

Choosing the right investment isn’t about picking the most popular stock or chasing the highest return. It’s about aligning your choices with your financial goals, personal comfort with risk, and how hands-on you want to be with managing your money. Here’s how to make an informed decision:

1. Define Your Financial Goals

Start by identifying what you’re investing for and when you’ll need the money. This helps determine the type of investment you should consider:

- Short-term (less than 3 years): Saving for a trip, emergency fund, upcoming tuition

→ Ideal options: High-yield savings accounts, certificates of deposit (CDs), government bonds - Medium-term (3–7 years): Saving for a car, wedding, or home down payment

→ Ideal options: Balanced mutual funds, robo-advisors, diversified ETFs - Long-term (7+ years): Retirement, wealth-building, child’s education

→ Ideal options: Index funds, stocks, REITs, retirement accounts (401k, IRA)

2. Assess Your Risk Tolerance

Everyone has a different comfort level with risk. Ask yourself:

- How would I react if my investments lost value temporarily?

- Am I willing to accept short-term losses for long-term gains?

- Do I prefer guaranteed returns, even if they’re lower?

Low risk tolerance: Consider bonds, savings accounts, CDs, or conservative funds

Moderate risk tolerance: Index funds, ETFs, robo-advisors

High risk tolerance: Individual stocks, REITs, or aggressive growth funds

3. Know How Much You Can Invest Regularly

Your monthly budget and cash flow play a big role in what you can afford to invest:

- Small, consistent amounts: Consider robo-advisors, micro-investing apps, or low-cost ETFs

- Lump-sum investment: You might have more access to mutual funds or CDs

- Irregular income: Use flexible platforms or invest whenever surplus cash is available

Tip: You don’t need a lot to start. Many platforms allow you to invest with as little as $5–$50/month.

4. Decide on Your Involvement Level

Are you interested in actively managing your investments, or do you prefer a “set it and forget it” approach?

- Passive investors (less time or knowledge):

→ Robo-advisors, index funds, retirement accounts - Active investors (want control or enjoy researching):

→ Individual stocks, sector-specific ETFs, REITs

If you’re unsure, start passively and learn as you go.

Final Tip: Start Simple

You don’t need to pick the “perfect” investment from day one. The most important step is starting. Choose a beginner-friendly option that suits your current goals and comfort level. You can always adjust your strategy as your income, knowledge, and confidence grow.

you may also like to read these posts:

Powerful & Compact: Best Portable Mini PCs for

Paghahanda para sa Pagsusulit: Gabay at Tips

Gabay Aral para sa mga Mag-aaral sa Elementarya

Rozmarra ki Budget Tips jo Asar Dikhayein

How to Start Investing: Step-by-Step Guide

Starting your investment journey doesn’t have to be overwhelming. Whether you’re investing $50 or $5,000, following a structured approach will help you build confidence and avoid common mistakes.

1. Set Up an Emergency Fund First

Before investing, make sure you have a financial safety net.

- Why? Investing carries risk, and your money shouldn’t be tied up if you suddenly need cash.

- How much? Aim for 3–6 months’ worth of essential expenses.

- Where to keep it? Use a high-yield savings account or money market account—safe, liquid, and accessible.

2. Open a Brokerage or Investment Account

To invest, you’ll need an account with access to financial markets.

- Brokerage account: Standard for buying stocks, ETFs, mutual funds

- Retirement account: 401(k), IRA, or Roth IRA (for long-term goals)

- Other options: Investment apps, robo-advisors, or traditional banks that offer investing services

Tip: Choose a platform with low fees, a clean interface, and beginner-friendly tools.

3. Choose Your Investment Platform

Pick the method that fits your knowledge, time, and preferences:

- Bank or credit union: Traditional and secure, but often limited options and higher fees

- Investment apps: Easy to use, low minimums (e.g., Robinhood, Public, Acorns, or your country’s equivalents)

- Robo-advisors: Automated investing based on your goals and risk profile (e.g., Betterment, Wealthfront)

- Online brokerages: Offer full control and access to many types of investments (e.g., Fidelity, Vanguard)

4. Decide Your Investment Amount and Frequency

- Start small: You don’t need a large sum—start with what you can afford.

- Be consistent: Set up monthly or biweekly contributions (called dollar-cost averaging).

- Balance your budget: Ensure investing doesn’t strain your ability to cover essentials.

Example: $100/month in a diversified ETF or index fund can grow significantly over time.

5. Monitor and Adjust Periodically

Investing isn’t one-and-done. Review your progress and make adjustments as needed.

- Check in monthly or quarterly

- Rebalance your portfolio annually if needed (adjust asset allocation based on goals and risk)

- As your income and goals evolve, increase your investment contributions

But avoid checking your investments daily—short-term market changes can be distracting and lead to impulsive decisions.

Common Mistakes to Avoid When Starting to Invest

Even with the best intentions, many beginner investors fall into traps that can cost them time, money, and confidence. Here are key mistakes to watch out for—and how to avoid them.

1. Following Trends Blindly

- The mistake: Jumping into investments because they’re trending on social media or getting hyped in the news.

- Why it’s risky: Trends often lead to buying high and selling low, especially when driven by speculation.

- Avoid it by: Doing your own research. Understand the business or asset you’re investing in and how it fits your goals and risk tolerance.

2. Not Understanding What You Invest In

- The mistake: Buying into a fund, stock, or crypto asset without knowing what it actually is or how it works.

- Why it’s risky: You can’t make informed decisions, manage risk, or evaluate performance if you don’t know what you own.

- Avoid it by: Sticking with simple, transparent investments at first—like index funds or ETFs—and learning as you go.

3. Trying to Time the Market

- The mistake: Waiting for the “perfect” time to invest or trying to buy low and sell high based on predictions.

- Why it’s risky: Even professionals rarely succeed at timing the market consistently. Delaying means missed compounding growth.

- Avoid it by: Investing consistently over time (dollar-cost averaging). Focus on time in the market, not timing the market.

4. Neglecting Fees and Taxes

- The mistake: Ignoring management fees, transaction charges, or tax consequences when choosing investments.

- Why it’s risky: Hidden fees and taxes can eat into your returns, especially over the long term.

- Avoid it by:

- Choosing low-cost index funds or ETFs

- Understanding the tax rules of your country (especially capital gains and dividends)

- Using tax-advantaged accounts when available (like IRAs or 401(k)s in the U.S.)

5. Investing Before Paying Off High-Interest Debt

- The mistake: Investing money while carrying high-interest credit card debt or personal loans.

- Why it’s risky: The interest on debt (e.g., 15–25%) can quickly outweigh the potential returns from investments.

- Avoid it by: Paying off high-interest debt first, then redirecting those monthly payments into your investment plan.

Final Tip:

Educate yourself before you invest. You don’t need to be an expert, but understanding the basics will help you make smarter, more confident decisions—and avoid costly missteps.

Faqs:

How much money do I need to start investing?

You can start investing with as little as $10 or even less, depending on the platform. Many apps now offer fractional shares, so you don’t need to buy full stocks to get started.

Is investing risky for beginners?

All investments carry some risk, but you can manage it by starting with low-risk options like index funds, government bonds, or high-yield savings accounts. The key is to invest based on your goals and risk tolerance.

Should I pay off debt before investing?

If you have high-interest debt (like credit cards), it’s usually best to pay that off first. However, you can still invest small amounts while paying down lower-interest loans.

What’s the difference between saving and investing?

Saving is for short-term goals and emergencies; it keeps your money safe but earns little interest. Investing is for long-term growth and involves risk, but it offers the potential for much higher returns over time.

What is the best investment option for beginners?

There’s no one-size-fits-all answer, but index funds, ETFs, and robo-advisors are often great starting points. They’re low-cost, diversified, and easy to manage, even for total beginners.

Conclusion

Investing may seem intimidating at first, but with the right mindset and a step-by-step approach, it can become one of the most powerful tools for building long-term wealth. Starting early—even with small amounts—gives your money more time to grow, thanks to the power of compound interest.

Remember:

- Focus on your personal financial goals, not market trends

- Choose investments that match your risk tolerance and timeline

- Build an emergency fund before investing

- Be consistent and patient—investing is a marathon, not a sprint

Avoid common pitfalls like chasing hype, neglecting fees, or investing without a plan. Instead, take the time to understand what you’re doing, start small, and grow your knowledge over time.

The most important step? Just start. The sooner you begin, the more time your money has to work for you.